kottke.org posts about economics

I think I’d heard the term “k-shaped economy” somewhere before but didn’t really know what it meant until I watched this video:

American Airlines is changing the layout of some of their aircraft to add 31 first class and premium seats while cutting out 73 economy seats. This is the hot new trend in air travel: pulling out all the stops to cater to the wealthy.

Airlines are adding suites with more bed space, privacy doors, an extra ottoman for guests. They’re offering caviar, free PJs, luxury skin care products, and multi-course meals with wine pairings made by gourmet chefs. They’re also building more airport lounges. Meanwhile, economy is getting more cramped and low-cost carriers are going bankrupt. It’s because wealthy passengers are where the money’s at.

For years, airlines have made more money from their credit cards than from actually flying passengers around. And these days, premium seating is bringing in more revenue than the economy cabin. It’s a perfect example of the K-shaped economy.

Here’s an AP article about the K-shaped economy from late last year.

Corporate executives are paying attention and in some cases explicitly adjusting their businesses to account for it. They are seeking ways to sell more high-priced items to the wealthy while also reducing package sizes and taking other steps to target struggling consumers.

Economist Thomas Piketty, writing for Le Monde (archive) on the success of Europe’s social democratic model and countering “the narrative of a ‘declining’ continent”:

If someone had told the European elites and liberal economists of 1914 that wealth redistribution would one day account for half of national income, they would have unanimously condemned the idea as collectivist madness and predicted the continent’s ruin. In reality, European countries have achieved unprecedented levels of prosperity and social well-being, largely due to collective investments in health, education and public infrastructure.

To win the cultural and intellectual battle, Europe must now assert its values and defend its model of development, fundamentally opposed to the nationalist-extractivist model championed by Donald Trump’s supporters in the United States and by Vladimir Putin’s allies in Russia. A crucial issue in this fight is the choice of indicators used to measure human progress.

For these indicators, Piketty mentions some of the same factors that economist Gabriel Zucman detailed in his Le Monde piece I posted in December:

More leisure time, better health outcomes, greater equality and lower carbon emissions, all with broadly comparable productivity: Europeans can be proud of their model, argues Gabriel Zucman, director of the EU Tax Observatory.

The main point of Adam Bonica’s post The Wall Looks Permanent Until It Falls is about the optimism of this moment: that the US could be ripe for a Berlin Wall-falling moment that opens the door for a better future. I’m not in the mood for that message these days (IMO, our Wall-falling is a ways off in the future), but Bonica’s analysis of how the US compares to 30 other wealthy democracies, our economic peers, is important.

Start with work and economic life. Americans work longer hours, pay more out-of-pocket for college and childcare, lack parental leave, and enjoy less economic mobility. The share of income going to the top 1 percent is nearly double the OECD average. American CEOs earn, on average, 354 times as much as their workers. More workers are trapped in poverty-wage jobs. Collective bargaining covers fewer workers. And social protections are less generous for those who fall on hard times, with the government raising less in taxes and spending more on the military.

The economy is just the beginning.

We spend nearly twice as much on healthcare as other wealthy countries do. Yet life expectancy is well below average, infant and maternal mortality rates are alarmingly high, and more Americans remain uninsured.

We suffer from overlapping public health crises — the highest rates of teenage births, drug overdoses, obesity, and gun deaths among peer nations.

His description of our unique exceptionalism goes on for several more paragraphs. But then he does something quite simple and revealing: he does the math and imagines, in concrete terms, what the US would be like if it were just an average country in its cohort. Bonica calls it “Latent America: the nation that would exist if our democracy functioned to serve the public rather than protect the already powerful”. Here’s part of his analysis:

I don’t think I’ve seen this analysis done in quite this way before. You should click through to see the whole graphic, but some of the other stats are:

- $19,000 added income per household per year (and $96K more wealth)

- $2.1 trillion less spending on healthcare

- 4.1 more years of life expectancy at birth

- 51 million more Americans voting

- 1.4 million fewer Americans behind bars

- 60 more women serving in Congress

And this is just if the US were an average nation. Imagine if the US took its exceptionalism seriously and tried to maximally improve the lives of its citizens & residents instead of generating, as Bonica puts it, “enormous prosperity while deliberately withholding it from those who need it most”.

In this video, Maurice Moves highlights a pair of flashlights that are extremely useful & well-designed but also shockingly affordable.

Most people never think about flashlights, but as someone who uses one daily for work, it’s always top of mind, and the tech, value, and products are proof that modern flashlights are absolutely insane and defy logic and manufacturing economics.

The two flashlights he featured are the WUBEN G5 Rechargeable EDC Flashlight ($20) and the Nitecore EDC37 8000 ($140) — the Wuben in particular would be affordable at twice the price given how nicely designed and engineered it is.

I feel like this about Apple’s M4 Macbook Airs; as I wrote last week, “$800 is an absurdly low price for so much computer”.

See also No One Knows How to Make a Pencil. (thx, dunstan)

Ryan Broderick on how, with the trade war that Trump’s tariffs has unleashed, we are speedrunning Brexit and other hyper-inflationary financial crises (thread) and Americans may soon find out what happens when US dollars don’t buy anything.

So from my uniquely weird perspective after living in the UK through Brexit, being in India during Modi’s demonetization, and living in Brazil when the real tanked during the Bolsonaro administration, I can confidently say that Americans do not and can not understand how bad this is going to be.

To sort of broadly describe what is about to happen if the Trump admin doesn’t reverse course, we are quickly racing towards a world where not only does our money just not work correctly anymore day to day, but the background radiation of a crumbling economy will become impossible to ignore.

After the Brexit referendum, everything in London just got slightly worse. A year or two in, you could feel it. But that’s because it took five years for the country to actually leave the EU. We’re speedrunning that. In Brazil, prices would change overnight, stores just wouldn’t have stuff.

There’s more; read the whole thing. Broderick was reacting to this brief WSJ piece (archive):

The broad selloff in U.S. stocks and bonds, and the continuing decline in the dollar, represents a “simultaneous collapse in the price of all U.S. assets,” analysts at Deutsche Bank said Wednesday. They warned that “unchartered territory” lies ahead.

- Markets are dedollarizing, they said, citing the lack of evidence that investors are hoarding dollar liquidity— a dynamic that in previous market routs fueled Treasury and U.S. dollar rallies but this time is leading to declines in the prices of both.

- The administration is encouraging the Treasury selloff, they said, in a bid to bring down U.S. asset valuations—a decision they said now is exposing the fact that “reducing bilateral trade imbalances is functionally equivalent to lowering demand for U.S. assets as well.”

- A financial war with China could lie ahead, they conclude, contending that “there is little room now left for an escalation on the trade front” and that “there can be no winner to such a war.”

I’ve been saying since his election that Trump was going to drive the economy into the ditch. This is more like driving it off a cliff.

A broad range of Americans are organizing a 24-hour economic boycott on February 28th to protest the ongoing actions of the Trump administration and to send a message to corporate America. From The People’s Union USA website, here are the details:

- The boycott runs all day on February 28th.

- People are urged to not make any purchases that day. No online shopping or in person.

- Do not spend money on: fast food, gas, or at major retailers. “No Amazon, no Walmart, no Best Buy.”

- If you need to buy essentials (food, medicine, emergency supplies), do so at small, local businesses and try to pay cash.

The idea is to show corporate America, using the thing they best understand (money), how much power Americans have when collectively organized. Organizers have billed this as an initial move (“if they don’t listen…we make the next blackout longer”) and have planned follow-up economic actions.

Awesome rabbit illustration by Martha Rich.

In a 1953 speech called On the Future of the American Negro, W.E.B. Du Bois spoke about wealth inequality and his vision for measuring prosperity:

Work is service, not gain. The object of work is life, not income. The reward of production is plenty, not private fortune. We should measure the prosperity of a nation not by the number of millionaires but by the absence of poverty, the prevalence of health, the efficiency of the public schools, and the number of people who can and do read worthwhile books.

Democracy Now has a recording of part of Du Bois’ speech (starting at 5:48).

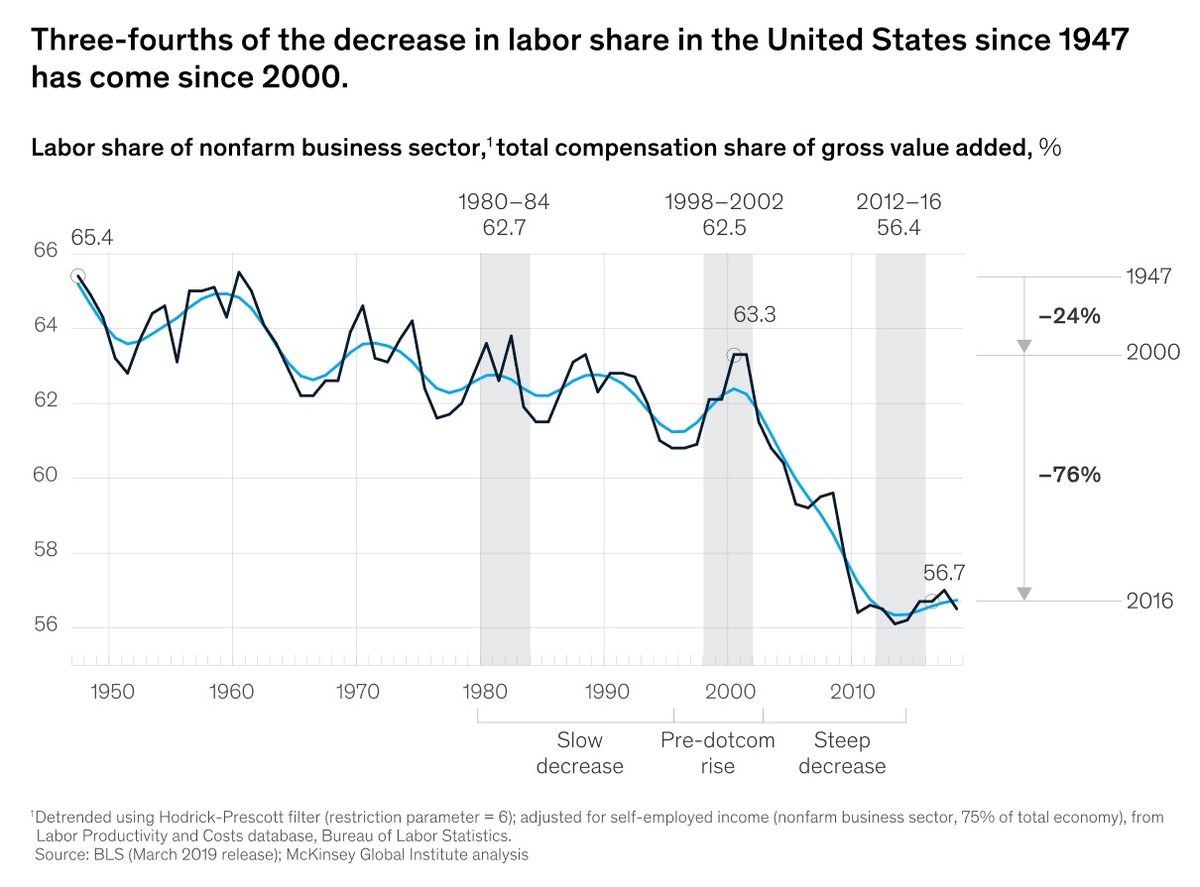

While listening to an episode of Scene on Radio’s excellent series on Capitalism, I learned about an economic measure called the labor share of national income. From The Guardian:

This week, the Bureau of Labor Statistics released its latest estimate for the share labor receives of national income for the first quarter of 2024. The statistics shows the income workers receive compared with the productivity their labor generates.

According to BLS, this income share has declined for non-farm workers from about two-thirds, 64.1% in the first quarter of 2001, to 55.8% in the first quarter of 2024.

Roughly speaking, in the first quarter of 2024, workers received ~56% of the income generated by their labor and 44% went to capital (ownership & shareholders).

Here’s a graph that shows the labor share of national income from 1947 to 2016 so you can get some idea of the decline that’s happened:

Scene on Radio hosts John Biewen and Ellen McGirt described labor share of national income like so:

Ellen McGirt: The labor share of national income. So, of all the income that businesses bring in, from sales of their goods and services, how much of that goes to workers. As opposed to, how much winds up as profits in the pockets of stockholders.

John Biewen: That number, according to the Federal Reserve, also went up significantly during the “thirty glorious years” in the United States. In the before times, in 1930, workers took home about 57% of the money that was generated by their labor. 57%. That labor share went up in the 1940s, to about 65% — almost two-thirds of corporate income was going to workers. It stayed over 60% for the next few decades, well into the 1970s.

Ellen McGirt: That doesn’t sound like a huge increase — from fifty-some percent to sixty-some percent. But the result, over those decades, was trillions of dollars in the pockets of people in the bottom 90-percent of the income scale — that’s money that would have gone to the wealthiest folks without those more progressive policies that reduced inequality. And then, guess what, starting in about 1975, the labor share of national income went down, and down. Until now, things are more like they were back in the days of Herbert Hoover.

This observation by McGirt is important but kind of hard to follow in text so I’ll restate it: when you’re talking about something as massive as the US economy, even a difference of a few percentage points in the labor share of national income over several years is trillions and trillions of dollars. And increasingly, those trillions are going to the wealthiest and not to the bottom 90%.

According to a groundbreaking new working paper by Carter C. Price and Kathryn Edwards of the RAND Corporation, had the more equitable income distributions of the three decades following World War II (1945 through 1974) merely held steady, the aggregate annual income of Americans earning below the 90th percentile would have been $2.5 trillion higher in the year 2018 alone. That is an amount equal to nearly 12 percent of GDP — enough to more than double median income — enough to pay every single working American in the bottom nine deciles an additional $1,144 a month. Every month. Every single year.

Price and Edwards calculate that the cumulative tab for our four-decade-long experiment in radical inequality had grown to over $47 trillion from 1975 through 2018. At a recent pace of about $2.5 trillion a year, that number we estimate crossed the $50 trillion mark by early 2020. That’s $50 trillion that would have gone into the paychecks of working Americans had inequality held constant — $50 trillion that would have built a far larger and more prosperous economy — $50 trillion that would have enabled the vast majority of Americans to enter this pandemic far more healthy, resilient, and financially secure.

From Adam Kovacs’ YouTube channel Adam Something comes this brisk 10-minute video essay on why European malls are doing better than their American progenitors. I thought his third point, about poor urban planning, was particularly interesting: malls tend to fail in America because they are not integrated into the fabric of towns and cities (because very little is integrated into the fabric of cities and towns in many places these days).

Malls, hell, all commerce has to be an organic part of towns and cities. People should be able to get to them by means other than a car, and conveniently. Such integrated commercial spaces are far more resilient. If your commercial spaces aren’t resilient — if you just plop a big box outside the town — don’t be surprised when it goes bust in a few years. And then it’s bulldozed for the next thing to be put up for it to go bust the same way and then get bulldozed and then the next thing and the next and the next so on and so forth.

For the past 13 years, former Secretary of Labor Robert Reich has taught a class called Wealth & Poverty at UC Berkeley. He retired from teaching this year and has uploaded his lectures from the course to YouTube.

Welcome to my final UC Berkeley course on Wealth and Poverty. Drawing on my 40+ years in politics, including my time as secretary of labor, I offer a deeper look at why inequalities of income and wealth have widened significantly since the late 1970s in the United States, and why this poses dangerous risks to our society.

This course also offers insights into the political and public-policy debates that have arisen in light of this inequality, as well as possible means of reversing it.

Here’s the first lecture, What’s Happened to Income & Wealth:

Reich has also published an abbreviated syllabus for each of the classes; links can be found in his course introduction (here’s class #1).

My pal Clive Thompson, who is in the midst of a two-part bicycle ride across the United States and is writing a book on micromobility, thinks local, state, and federal governments should start offering substantial subsidies for e-bikes in order to help reduce car usage, decrease urban pollution, and to lower the cost of transportation for lower-income families.

The thing is, we should lean heavily into subsidies for electric bikes — now.

If Denver’s experience is any guide, it’d be a huge boon for town, cities, and even many suburbs. Ebikes can’t be used to replace all car travel, of course; but as folks who experiment with them discover, wow, you start leaving your car at home a lot. If towns and cities are smart about how they organize and issue these credits, they can also help lower-income families add much cheaper mobility to their transportation options. Denver found that low-income-qualified folks who bought ebikes rode them almost 50% more than other voucher-getters, probably because the ebike became, hands-down, their most affordable way to travel.

We’re also not talking about a ton of money here. Ebike subsidies are considerably cheaper than those for cars or solar arrays. Even a few hundred bucks of subsidy per e-bike could help drop the price down to something competitive with a regular pedal bike. If all three levels of government worked together — federal, state, and local — the US could find the money for an absolute ton of ebike support, I suspect. (We could also consider reallocating some of the estimated $20 billion in annual subsidies that US taxpayers currently hand out to oil and gas companies.)

Hear, hear. I recently bought an e-bike (more on that in a future post) and went online looking for local subsidies. Vermont had an e-bike incentive program that ran for barely two months in 2022:

The eBike Incentive Program launched July 21, 2022, but closed shortly afterwards on September 16, 2022 when the $105,000 authorized in program funding was exhausted. Vermont residents aged 16 or older were eligible on a first-come, first-served basis for up to $400 towards the purchase of an electric bicycle, with higher incentives for households and individuals with lower incomes.

Bummer. The local power company offers $200 rebates though, which is nice.

Update: Vermont just refreshed their incentive program with an additional $150,000 a few days ago. Huzzah! (thx, rintze)

Expanding on his previous thoughts on the relationship between AI and capitalism — “I tend to think that most fears about A.I. are best understood as fears about capitalism” — Ted Chiang offers a useful metaphor for how to think about AI: as a management-consulting firm like McKinsey.

So, I would like to propose another metaphor for the risks of artificial intelligence. I suggest that we think about A.I. as a management-consulting firm, along the lines of McKinsey & Company. Firms like McKinsey are hired for a wide variety of reasons, and A.I. systems are used for many reasons, too. But the similarities between McKinsey — a consulting firm that works with ninety per cent of the Fortune 100 — and A.I. are also clear. Social-media companies use machine learning to keep users glued to their feeds. In a similar way, Purdue Pharma used McKinsey to figure out how to “turbocharge” sales of OxyContin during the opioid epidemic. Just as A.I. promises to offer managers a cheap replacement for human workers, so McKinsey and similar firms helped normalize the practice of mass layoffs as a way of increasing stock prices and executive compensation, contributing to the destruction of the middle class in America.

A former McKinsey employee has described the company as “capital’s willing executioners”: if you want something done but don’t want to get your hands dirty, McKinsey will do it for you. That escape from accountability is one of the most valuable services that management consultancies provide. Bosses have certain goals, but don’t want to be blamed for doing what’s necessary to achieve those goals; by hiring consultants, management can say that they were just following independent, expert advice. Even in its current rudimentary form, A.I. has become a way for a company to evade responsibility by saying that it’s just doing what “the algorithm” says, even though it was the company that commissioned the algorithm in the first place.

Good stuff — I especially enjoyed the mini You’re Wrong About on the Luddites — do read the whole thing.

From Vox, an inflation explainer video that sums up the three primary explanations for the current rise in prices worldwide — Too much money, supply shocks, massive markups (aka corporate price gouging) — and what governments can do about it.

Right now, inflation is inescapable. At the grocery store, the gas station, and in almost every country in the world, people are playing more — way more — than they did just a couple of years ago for everything.

In this video, we explore three explanations for why prices are rising, as well as different policy options for bringing them down.

Genetics determines most of how tall children will grow as adults, but environmental factors affect it too. As the wealth of many countries around the world has increased over the past 100 years, living conditions and access to nutrition have improved and people have gotten taller.

A century ago, humans were quite short. For example, the average South Korean woman was about 4-foot-7, or 142 centimeters, while the average American woman was about 5-foot-2, or 159 centimeters. Humans were fairly short by today’s standards, and that was true throughout nearly all of human history.

But in the past century, human heights have skyrocketed. Globally, humans grew about 3 inches on average, but in South Korea, women grew an astounding 8 inches and men grew 6 inches.

South Korea is almost unique in how quickly their population has gotten taller because they went from a relatively low-income country in the 1950s to well on their way to being a rich, industrialized country by the 90s. And the difference is particularly stark when you compare the heights of South Koreans with those of North Koreans, where the living standard is much lower and access to nutrition is restricted.

I really like the show-your-work vibe of this video, along with this recent one on the greatest unexpected performances in the NBA. These videos are not only relating something interesting to the audience, they’re showing us how the data analysis works: where the data is from, how it’s analyzed, and what it all means, which builds data and statistical literacy in a society that desperately needs it.

Eric Huang is the chef/owner/operator of Brooklyn’s lauded Pecking House fried chicken joint. In a recent Instagram post, Huang explains why tipping is a part of the experience at his restaurant.

We do NOT use a tip credit at Pecking House. If we do not take a tip credit that means we pay every employee at least $15/hour. We then pool the tips and divide them among the entire hourly staff, including all back-of-house employees. This helps to foster an equitable team culture where everyone feels they are participating in the restaurant’s success.

So far, we’ve been able to pay every front-line employee an average of an extra $7 per hour on top of their hourly wages. We’ve been managing that while collecting a tip average of 18% on a check average of $26. So even an entry-level employee at Pecking House is making $22/hour if not more.

Almost no one in New York City does this. This is pretty damn unique. And while people have been generally enthusiastic about supporting restaurants as they weather a furious storm of inflation, this is an easy way for us to take better care of our restaurant workers. Because the pandemic revealed quite painfully that we are a sizable, important and vulnerable population. And this is all perhaps even more relevant given that certain Best Restaurants have been outed about certain abhorrent business practices. Their example should be motivating us to take a look at how we can change the restaurant industry for the better.

So when you add a tip at Pecking House, you’re really helping to take care of the whole team and acknowledge their effort in creating your experience. I think we’ve all been guilty of having a great time and leaving a fat tip, but forgetting at that moment that the cook who made you that taglioni isn’t seeing an extra penny. So for those of you who have been helping us out with 18% on $26, an extra $4, know that it’s going to everyone. Except and rightfully so, the chef standing there pointing at stuff, not being terribly helpful, i.e. me.

From there, he goes on to explain why eliminating tipping doesn’t work from the standpoint of the restaurant (customers spend less), its employees (they make less than they could elsewhere), or, surprisingly, its customers (they want the illusion of control/agency). And there’s also a sort of tacit collusion that happens amongst restaurants — no one wants to eliminate this obviously unfair system because of the financial hit so none of them do. The whole thing is worth a read.

Back when I lived in NYC, a restaurant I frequented experimented for a few months with eliminating tipping. In practice, it meant that the bartenders and servers made less money and the chefs got paid more. As a regular customer who knew and liked everyone who worked there, I thought that was much more fair than front-of-the-house staff being paid more than the kitchen folks due to some antiquated racist bullshit. In the end, they had to revert to doing tips again because customers weren’t spending as much money and it eliminated the restaurant’s profit margin. Customers looked at the higher prices ($25 for the chicken instead of $21, $17 cocktails instead of $14) and ordered fewer and less-expensive items, even though they were paying exactly the same amount for them by tacking 20% onto the check at meal’s end. It’s just economic reality: lower posted prices with added fees will encourage people to spend more money because the posted price is what gets stuck in their heads.

It seems like the only way to get rid of tipping in the US is for every restaurant to do it simultaneously, either by mutual decision (ha!) or through some kind of legislation (double ha!). But because of the pandemic and the ubiquity of digital payment screens, tipping is more engrained in American commerce than ever so…??

See also The Failure of the Great Tip-Free Restaurant Experiment.

I’ve never heard this theory before: L. Frank Baum wrote The Wizard of Oz as an allegory for the 1896 Presidential election, the central issue of which was the monetary concept of bimetallism. Quickly, from Wikipedia, a definition of bimetallism:

Bimetallism is a monetary standard in which the value of the monetary unit is defined as equivalent to certain quantities of two metals, typically gold and silver, creating a fixed rate of exchange between them.

There was much debate in the run-up to the election over how to define the rate between gold and silver in the US. Here’s where The Wizard of Oz comes in:

Dorothy is whipped out of Kansas by a tornado with her little dog “Toto” (short for teetotalers, who made a loud noise yip-yapping but were otherwise ineffective political companions). On her way to the Land of Oz, Dorothy picks up her electoral coalition. First, the Scarecrow, representing western farmers. “He thinks that he has no brains because his head is stuffed with straw. But we soon learn that he is shrewd and capable. He brings to life a major theme of the free silver movement: that the people, the farmer in particular, were capable of understanding the complex theories that underlay the choice of a standard.”

Next, the Tin Man (or Tin Woodman). The working class man, once a true human, is now just a cog in the industrial machine. Piece by piece his human body was replaced by metallic parts. He is now little more than a machine, a heartless (literally) machine. The Populist hope of the era was a grand farmer-labor coalition that never quite solidified — and we still see residual evidence of this hope in the official name of Minnesota’s Democratic Party, the Democratic-Farmer-Labor Party.

The Cowardly Lion, then, was William Jennings Bryan himself. Capable of a great roar — his speeches were legendary — alas, to mix metaphors, he was all bark and no bite.

(via kyle westaway)

Starbucks sells coffee. But you can also think of Starbucks as a bank — and an unregulated one at that. As part of their rewards program, millions of Starbucks customers have preloaded money onto Starbucks cards, essentially loaning the company more than $1 billion at 0% interest.

Starbucks has around $1.6 billion in stored value card liabilities outstanding. This represents the sum of all physical gift cards held in customer’s wallets as well as the digital value of electronic balances held in the Starbucks Mobile App.* It amounts to ~6% of all of the company’s liabilities.

This is a pretty incredible number. Stored value card liabilities are the money that you, oh loyal Starbucks customer, use to buy coffee. What you might not realize is that these balances simultaneously function as a loan to Starbucks. Starbucks doesn’t pay any interest on balances held in the Starbucks app or gift cards. You, the loyal customer, are providing the company with free debt.

See also McDonald’s is a real estate company.

Anne Helen Peterson noticed a bunch of reports about fast food & retail businesses around the US having trouble finding employees, which difficulty the business owners are blaming on lazy American workers whose unemployment benefits have been extended/expanded during the pandemic. But what if, she writes, those benefits are actually providing a safety net to American workers so that they do not need to take terrible jobs for low wages at terrible companies under terrible management? The ‘Capitalism is Broken’ Economy:

Stick with me here, but what if people weren’t lazy — and instead, for the first time in a long time, were able to say no to exploitative working conditions and poverty-level wages? And what if business owners are scandalized, dismayed, frustrated, or bewildered by this scenario because their pre-pandemic business models were predicated on a steady stream of non-unionized labor with no other options? It’s not the labor force that’s breaking. It’s the economic model.

Unemployment benefits have offered a steady paycheck while you figure out your options. Put differently: a version of the safety net that’s been missing from most American employment, and, by extension, the ability to say no. No, I don’t have to work for a restaurant that only gives me my hours three days ahead of time, thus making it nearly impossible to find reliable childcare. No, I don’t have to work clopen shifts. No, I don’t have to expect a job without sick leave or paid time off. No, I don’t have to deal with asshole customers or managers who degrade me without consequence. No, I don’t have to work in a job with significant, accumulating health risks.

Her question near the end of the piece is worth considering: “If a business can’t pay a living wage, should it be a business?”

Last week, twelve of the biggest, richest, and best European soccer teams announced they were going to form a new midweek competition called The European Super League. The reaction was swift: fans revolted, soccer governing bodies threatened to kick these teams out of other competitions (with immediate effect, including the Champions League which is presently in the semifinal stage), large-scale condemnation from the press, teams started to back out, and 48 hours after the announcement, the league was all but dead.

So what the hell happened? There have been lots of takes and I obviously haven’t read them all, but here are two I found especially valuable in wrapping my head about the Super League failure and, more importantly, what it can tell us about how power, wealth, community, and attention interact 21 years into this rapidly aging century. First up, Alex Shephard writing for The New Republic: The Existential Crisis That Led to the European Super League Fiasco.

What all of these cultural dinosaurs are confronting, though rarely head on, is the fact that there is no monoculture anymore. They may occupy tremendous cultural space — and a team like Real Madrid is rivaled only by other European soccer teams in the sports world — but it is not and never will be what it was before. The mass appeal these teams enjoyed until fairly recently is not coming back, and it’s not just the fault of Fortnite or FIFA. There are simply too many competitors — and, after all, you can watch the best bits on social media anyways.

And then Ryan O’Hanlon interviewed economist Mark Blyth for his newsletter: How the Spectacular, Comical Failure of the Super League Explains the World.

O’Hanlon: In addition to the various corporate pressures, it really does seem like the fan reaction made a material difference. Do you find that heartening at all?

Blyth: I think it’s heartening in the following sense. It’s emblematic of broader shifts that are going on right now. Basically we’re all struggling to find a capitalism 4.0, and we’re all fed up with capitalism 3.0, and this is a huge example of the limits of capitalism 3.0. This “I own it. It’s my right. I’ll do what I want with it”. Except, no you won’t because there’s such a thing as a public conception of ownership of these assets, even if you formally own them. There are limits to how far you can push this market logic on the social institutions without provoking a reaction. Karl Polanyi, the Hungarian sociologist and historian from the 1940s, wrote that the big fuck-ups of the 19th century and 20th century were attempts to shove markets down people’s throats to the point where they revolted.

In a sense, what you’re seeing here is a classic Polanyian reaction. So I think it’s heartening in that it shows there are limits to how much you can commodify these social goods even if they are nominally private assets. It’s heartening in another way in that they’re gonna have to have a reckoning with these balance sheets. If you’re not Sheikh Mansour and you’re not Roman Abramovich, how are you going to fund Paul Pogba’s ridiculous salary? And it’s just not clear that you are going to, so there may need to be a restructuring, which would be great because the model is there. Look at how the Germans do this. They invest heavily in talent. They invest heavily in youth, they buy, but they buy judiciously. They don’t pay ludicrous salaries. And the funds own 51 percent of the companies. It’s a perfect model, right? Because they’ve got cooperative ownership between the people who are the kind of social owners. And then you’ve got the titular owners who do the investment, and there’s a balance of those interests.

Let me know if there are other Super League pieces out there that I should read — I’ll add them to this post. (Photo above of Erling Haaland because he is a goofy beast and one of the 12 Super League teams is going to pay an absolutely obscene amount of money for him in a few months.)

Writer Ted Chiang (author of the fantastic Exhalation) was recently a guest on the Ezra Klein Show. The conversation ranged widely — I enjoyed his thoughts on superheroes — but his comments on capitalism and technology seem particularly relevant right now. From the transcript:

I tend to think that most fears about A.I. are best understood as fears about capitalism. And I think that this is actually true of most fears of technology, too. Most of our fears or anxieties about technology are best understood as fears or anxiety about how capitalism will use technology against us. And technology and capitalism have been so closely intertwined that it’s hard to distinguish the two.

Let’s think about it this way. How much would we fear any technology, whether A.I. or some other technology, how much would you fear it if we lived in a world that was a lot like Denmark or if the entire world was run sort of on the principles of one of the Scandinavian countries? There’s universal health care. Everyone has child care, free college maybe. And maybe there’s some version of universal basic income there.

Now if the entire world operates according to — is run on those principles, how much do you worry about a new technology then? I think much, much less than we do now. Most of the things that we worry about under the mode of capitalism that the U.S practices, that is going to put people out of work, that is going to make people’s lives harder, because corporations will see it as a way to increase their profits and reduce their costs. It’s not intrinsic to that technology. It’s not that technology fundamentally is about putting people out of work.

It’s capitalism that wants to reduce costs and reduce costs by laying people off. It’s not that like all technology suddenly becomes benign in this world. But it’s like, in a world where we have really strong social safety nets, then you could maybe actually evaluate sort of the pros and cons of technology as a technology, as opposed to seeing it through how capitalism is going to use it against us. How are giant corporations going to use this to increase their profits at our expense?

And so, I feel like that is kind of the unexamined assumption in a lot of discussions about the inevitability of technological change and technologically-induced unemployment. Those are fundamentally about capitalism and the fact that we are sort of unable to question capitalism. We take it as an assumption that it will always exist and that we will never escape it. And that’s sort of the background radiation that we are all having to live with. But yeah, I’d like us to be able to separate an evaluation of the merits and drawbacks of technology from the framework of capitalism.

Echoing some of his other thoughts during the podcast, Chiang also wrote a piece for the New Yorker the other day about how the singularity will probably never come.

Buried deep within Jamie Lauren Keiles’ NY Times article about frequent flyer miles and The Points Guy is this economic observation:

A major reason points-and-miles trips exist is because airlines turn a more stable profit by minting their own currencies than by selling actual airline seats. The flight seems almost ancillary to the financial transaction it enables — a trend across the whole economy, where the selling of goods or services serves to enable the collection of data, the absorption of venture capital funds or the levying of hidden transaction fees. In this scheme, posting to social media, or collecting points and miles, or ordering a taxi or a gyro on your phone, is merely a gesture to keep the whole process in motion. The real moneymaking happens behind the scenes, driven by a series of exchanges where value seems conjured from nothing at all.

But of course, value always comes from somewhere. If you trace the thread back on any one of these businesses, it’s always the same deal: The poor underwrite the fantasies of the middle class, who in turn underwrite the realities of the rich. When credit cards charge high interchange fees, they pass the cost of loyalty programs on to merchants, who in turn pass it back to customers by building the fees into their sticker prices. Those who pay with credit can earn it back in points. Those who pay with debit or cash wind up subsidizing someone else’s free vacation. According to a 2010 policy paper by economists at the Federal Reserve Bank of Boston, the average cash-using household paid $149 over the course of a year to card-using households, while each card-using household received $1,133 from cash users, partially in the form of rewards. It remains a regressive transfer to this day.

Emphasis of the second to last sentence is mine.

Trickle-down economics is the economic theory that lowering taxes on the wealthy and on businesses will stimulate business investment to the long-term benefit of society. The idea is that by sprinkling a huge amount of money into the bank accounts and stock portfolios of the wealthy, a portion of that money will “trickle down” to everyone else. Despite ample evidence that it hasn’t worked, trickle-down has been an economic driver for discussions about taxes in the US since at least the Reagan administration. The newest research that argues that tax cuts for the rich don’t work for anyone other than the rich comes in the form of working paper by David Hope of the London School of Economics and Julian Limberg of King’s College London called The Economic Consequences of Major Tax Cuts for the Rich. From the press release:

Our results show that…major tax cuts for the rich increase the top 1% share of pre-tax national income in the years following the reform. The magnitude of the effect is sizeable; on average, each major reform leads to a rise in top 1% share of pre-tax national income of 0.8 percentage points. The results also show that economic performance, as measured by real GDP per capita and the unemployment rate, is not significantly affected by major tax cuts for the rich. The estimated effects for these variables are statistically indistinguishable from zero.

And the authors’ conclusion:

Our results have important implications for current debates around the economic consequences of taxing the rich, as they provide causal evidence that supports the growing pool of evidence from correlational studies that cutting taxes on the rich increases top income shares, but has little effect on economic performance.

Limberg connected the results of the research to post-pandemic economic recovery:

Our results might be welcome news for governments as they seek to repair the public finances after the COVID-19 crisis, as they imply that they should not be unduly concerned about the economic consequences of higher taxes on the rich.

Former US Labor Secretary Robert Reich agrees that the US should tax the rich to invest in public infrastructure.

The practical alternative to trickle-down economics might be called build-up economics. Not only should the rich pay for today’s devastating crisis but they should also invest in the public’s long-term wellbeing. The rich themselves would benefit from doing so, as would everyone else.

At one time, America’s major political parties were on the way to embodying these two theories. Speaking to the Democratic national convention in 1896, populist William Jennings Bryan noted: “There are two ideas of government. There are those who believe that, if you will only legislate to make the well-to-do prosperous, their prosperity will leak through on those below. The Democratic idea, however, has been that if you legislate to make the masses prosperous, their prosperity will find its way up through every class which rests upon them.”

Build-up economics reached its zenith in the decades after the second world war, when the richest Americans paid a marginal income tax rate of between 70% and 90%. That revenue helped fund massive investment in infrastructure, education, health and basic research — creating the largest and most productive middle class the world had ever seen.

In a piece for the NY Times called What Is Owed, Nikole Hannah-Jones argues that because of its sanction of slavery and subsequent legalized racial segregation and discrimination, it is time for the United States government to pay its debt to Black Americans in form of reparations.

To summarize, none of the actions we are told black people must take if they want to “lift themselves” out of poverty and gain financial stability — not marrying, not getting educated, not saving more, not owning a home — can mitigate 400 years of racialized plundering. Wealth begets wealth, and white Americans have had centuries of government assistance to accumulate wealth, while the government has for the vast history of this country worked against black Americans doing the same.

“The cause of the gap must be found in the structural characteristics of the American economy, heavily infused at every point with both an inheritance of racism and the ongoing authority of white supremacy,” the authors of the Duke study write. “There are no actions that black Americans can take unilaterally that will have much of an effect on reducing the wealth gap. For the gap to be closed, America must undergo a vast social transformation produced by the adoption of bold national policies.”

This piece is one of the best things I’ve read this year. It is clear, focused, powerful, and persuasive. There is no amount of money that anyone could ever pay to make up for the 400+ years of absolute shit rained down on Black people by the United States of America and its precursors, but nevertheless, reparations are the only just and moral way forward for the United States.

P.S. Here’s the Duke study mentioned in the excerpt above: What We Get Wrong About Closing the Racial Wealth Gap. And the book containing a detailed plan for reparations mentioned by Hannah-Jones is From Here to Equality: Reparations for Black Americans in the Twenty-First Century (ebook).

Update: Terry Gross interviewed Hannah-Jones on Fresh Air about reparations.

I think that reparations can’t just be any one thing. I think that you have to have targeted investment in Black communities and Black schools that have been generationally under-resourced. You certainly need to have a commitment to strong enforcement of existing civil rights laws, because reparations don’t do any good if you’re still facing rampant employment and housing and educational discrimination. But the center of any reparations program has to be cash payments. The only thing that closes a wealth gap is money.

For Slate’s 2015 podcast series The History of American Slavery, Andrew Kahn created an interactive visualization of the 20,000+ voyages that made up the Atlantic slave trade that lasted 315 years. A video of the interactive map is embedded above.

As we discussed in Episode 2 of Slate’s History of American Slavery Academy, relative to the entire slave trade, North America was a bit player. From the trade’s beginning in the 16th century to its conclusion in the 19th, slave merchants brought the vast majority of enslaved Africans to two places: the Caribbean and Brazil. Of the more than 10 million enslaved Africans to eventually reach the Western Hemisphere, just 388,747 — less than 4 percent of the total — came to North America. This was dwarfed by the 1.3 million brought to Spanish Central America, the 4 million brought to British, French, Dutch, and Danish holdings in the Caribbean, and the 4.8 million brought to Brazil.

Roughly 400,000 enslaved Africans were brought to the United States before the practice was banned in 1808. The ban was mostly (but not entirely) enforced and yet in 1860, the population of enslaved persons was almost 4 million in the South. That’s because the 1808 ban, according to Ned & Constance Sublette’s book The American Slave Coast: A History of the Slave-Breeding Industry, was a form of trade protectionism that protected the forced breeding of enslaved peoples by American slaveowners. From a review of the book:

In fact, most American slaves were not kidnapped on another continent. Though over 12.7 million Africans were forced onto ships to the Western hemisphere, estimates only have 400,000-500,000 landing in present-day America. How then to account for the four million black slaves who were tilling fields in 1860? “The South,” the Sublettes write, “did not only produce tobacco, rice, sugar, and cotton as commodities for sale; it produced people.” Slavers called slave-breeding “natural increase,” but there was nothing natural about producing slaves; it took scientific management. Thomas Jefferson bragged to George Washington that the birth of black children was increasing Virginia’s capital stock by four percent annually.

Here is how the American slave-breeding industry worked, according to the Sublettes: Some states (most importantly Virginia) produced slaves as their main domestic crop. The price of slaves was anchored by industry in other states that consumed slaves in the production of rice and sugar, and constant territorial expansion. As long as the slave power continued to grow, breeders could literally bank on future demand and increasing prices. That made slaves not just a commodity, but the closest thing to money that white breeders had. It’s hard to quantify just how valuable people were as commodities, but the Sublettes try to convey it: By a conservative estimate, in 1860 the total value of American slaves was $4 billion, far more than the gold and silver then circulating nationally ($228.3 million, “most of it in the North,” the authors add), total currency ($435.4 million), and even the value of the South’s total farmland ($1.92 billion). Slaves were, to slavers, worth more than everything else they could imagine combined.

You can read more about the economics of slavery in this post from 2016, including how American banks sold bonds that used enslaved persons as collateral to international investors. (via open culture)

In this video for NPR, Gene Demby summarizes the history of housing segregation in America and how it’s a factor for current differences in health (poorer), wealth (much less), education (underfunded), and policing (much more aggressive) for Black communities in US cities.

If you look at the way housing segregation works in America, you can see how things ended up this way. Once you see it, you won’t be able to unsee it.

When you’re talking about housing policy in America, Kimberly Jones’ Monopoly analogy starts to sound a lot less metaphorical and more literal: if Black people cannot buy houses or can only buy houses on certain streets, they will not be able to build wealth like others can.

For more on housing segregation, check out historian Richard Rothstein’s The Color of Law: A Forgotten History of How Our Government Segregated America. From a 2017 interview with Rothstein:

The federal government pursued two important policies in the mid-20th century that segregated metropolitan areas. One was the first civilian public housing program which frequently demolished integrated neighborhoods in order to create segregated public housing.

The second program that the federal government pursued was to subsidize the development of suburbs on a condition that they be only sold to white families and that the homes in those suburbs had deeds that prohibited resale to African-Americans. These two policies worked together to segregate metropolitan areas in ways that they otherwise would never have been segregated.

Rothstein talked about the book with Ta-Nehisi Coates during a conversation at Politics and Prose Bookstore.

Update: This is excellent: you can explore the maps created by the federal government’s Home Owners’ Loan Corporation at Mapping Inequality by the University of Richmond’s Digital Scholarship Lab.

These grades were a tool for redlining: making it difficult or impossible for people in certain areas to access mortgage financing and thus become homeowners. Redlining directed both public and private capital to native-born white families and away from African American and immigrant families. As homeownership was arguably the most significant means of intergenerational wealth building in the United States in the twentieth century, these redlining practices from eight decades ago had long-term effects in creating wealth inequalities that we still see today.

(via @masonadams)

Do me a favor and take about 7 minutes to watch author Kimberly Jones’ off-the-cuff “rant” (her words) about how rioting and looting fit within the larger narrative of the economic oppression of Black people in America. I’ve never heard the long, shameful, and deadly history of white supremacy in America summed up any better or more succinctly than Jones does here. The Monopoly analogy in particular is fantastic.

When they say “Why do you burn down the community? Why do you burn down your own neighborhood?” It’s not ours! We don’t own anything! We don’t own anything! Trevor Noah said it so beautifully last night: There’s a social contract that we all have — that if you steal or if I steal, then the person who is the authority comes in and they fix the situation. But the person who fixes the situation is killing us! So the social contract is broken. And if the social contract is broken, why the fuck do I give a shit about burning the fucking Football Hall of Fame, about burning the fucking Target? You broke the contract when you killed us in the streets and didn’t give a fuck! You broke the contract when for 400 years we played your game and built your wealth!

Update: Jones has signed a deal with Henry Holt and Company to write two books, one of which will be called “How We Can Win” and will be based on the video above.

Update: How We Can Win will be out in November and is now available for preorder.

From an April 17th Facebook post by Paul Field, a succinct summary of how the pandemic exposes American deficiencies. It’s tough to not just quote the whole thing, so here’s the beginning:

Everyone is entitled to their own opinion, but you need to know how silly you look if you post some variation of, “Welcome to Socialism…”

You are not seeing Socialism. What you are seeing is one of the wealthiest, geographically advantaged, productive capitalist societies in the world flounder and fail at its most basic test. Taking care of its people.

This crisis is not about the virus.

This crisis is about the massive failure of our, “Booming economy,” to survive even modest challenges. It is about the market dissonance of shortages in stores, even as farmers/producers destroy unused crops and products. This crisis is about huge corporations needing an emergency bailout within days of the longest Bull Market in our history ending and despite the ability to borrow with zero percent interest rates.

The pandemic has revealed that American democracy and our economic system is extremely fragile. Ok, unless you’re wealthy, in which case you’re going to be fine, all part of the plan, etc.

This too-short profile of Pulitzer Prize-winning journalist Laurie Garrett, who has been writing about epidemics since the 90s, is closer to my personal feelings as to how the pandemic plays out in the US than almost anything else I’ve read.

But she can’t envision that vaccine anytime in the next year, while Covid-19 will remain a crisis much longer than that.

“I’ve been telling everybody that my event horizon is about 36 months, and that’s my best-case scenario,” she said.

“I’m quite certain that this is going to go in waves,” she added. “It won’t be a tsunami that comes across America all at once and then retreats all at once. It will be micro-waves that shoot up in Des Moines and then in New Orleans and then in Houston and so on, and it’s going to affect how people think about all kinds of things.”

They’ll re-evaluate the importance of travel. They’ll reassess their use of mass transit. They’ll revisit the need for face-to-face business meetings. They’ll reappraise having their kids go to college out of state.

Much of the federal government’s response has been to help big business, and the wealthy are going to have opportunities to not only ride out the storm more easily but to take advantage:

If America enters the next wave of coronavirus infections “with the wealthy having gotten somehow wealthier off this pandemic by hedging, by shorting, by doing all the nasty things that they do, and we come out of our rabbit holes and realize, ‘Oh, my God, it’s not just that everyone I love is unemployed or underemployed and can’t make their maintenance or their mortgage payments or their rent payments, but now all of a sudden those jerks that were flying around in private helicopters are now flying on private personal jets and they own an island that they go to and they don’t care whether or not our streets are safe,’ then I think we could have massive political disruption.”

I could quote something from just about every paragraph, but for now I’ll just do one more excerpt and you can go and read the rest.

Garrett recounted her time at Harvard. “The medical school is all marble, with these grand columns,” she said. “The school of public health is this funky building, the ugliest possible architecture, with the ceilings falling in.”

“That’s America?” I asked.

“That’s America,” she said.

See also Dave Eggers’ pandemic Q&A, which shares a certain pessimistic honesty with Garrett’s thoughts.

Using data from the Correlates of War Project and the Stockholm International Peace Research Institute, this bar chart race shows the annual military spending of the world’s top spending countries from the start of WWI in 1914 to 2018. See also military spending info from Our World in Data.

In early March, Dr. Caroline Schulman was responsible for calling patients at her hospital to tell them they had tested positive for Covid-19. She shared some of her experiences in a piece for Stat.

Erik lives with his entire family in a one-room rental house with eight other occupants. He didn’t understand the precautions for preventing the spread of Covid-19 and had regularly been socializing in the apartment. He kept asking how to file for unemployment and how to isolate the household when the house itself could barely hold those living in it.

Jeff lives alone. He has a chronic blood condition and is struggling to get by. A few hours before we talked, he had resumed his job as a ride share driver because he needed to make ends meet.

Angela is 40 years old and has one of the preexisting conditions that put people at high risk for serious complications of Covid-19. When we spoke, she told me that she was feeling better, but that her home life was difficult. Her children had returned home after Mayor Muriel Bowser issued a stay-at-home order for the District of Columbia. She asked her kids to take precautions, but they continued to leave the house often. One son brought home his girlfriend, who had a cough, and displaced Angela from her room. She was unable to make an appointment with her primary doctor and couldn’t afford her medical supplies because of insurance issues. When I spoke with her, she sounded well and had no classic symptoms, but something didn’t sound right. I arranged a televisit that afternoon to have her evaluated more closely. By the time she got the call two hours later, she was so short of breath she could barely speak. When an ambulance arrived to take her to the hospital, her oxygen levels were dangerously low.

Reading through these stories, I just kept thinking about the measures that are going to be necessary if we’re going to safely restart public life in America — hygiene, mask wearing, some social distancing, and eventually a vaccine — and how our collective safety is going to depend on individuals doing the right thing. And most people will. But it’s clear that, especially without coherent national leadership & economic support, some people will be unable to take the necessary precautions for economic reasons and others won’t because they don’t understand why these measures are necessary, don’t trust science, or a dozen other reasons.

Older posts

Socials & More